This article is republished from chinadialogue.

Generous subsidies have been slashed or removed to rein in rampant growth. Liu Bin examines the changes

Solar powered photovoltaic cells are assembled by workers at a factory in Dezhou, Shandong province (Image: Greenpeace/Alex Hofford)

China’s solar manufacturers are unhappy with recent government policy changes that have put a brake on the sector.

“We’ve already halted work on 11 megawatts of industrial and commercial distributed solar PV projects,” says the marketing director for one solar photovoltaic (PV) module manufacturer in Guangdong province.

“Without subsidies there’s no return on investment for over a decade, so investors and property owners aren’t interested in distributed solar. With subsidies it only takes seven years to recoup the investment,” he adds.

This is one consequence of China’s “531” policy that was announced by the National Development and Reform Commission, the Ministry of Finance, and the National Energy Administration without warning on May 31(hence the “531” name). The policy is designed to control breakneck growth in the solar sector, principally by accelerating the phase-out of subsidies.

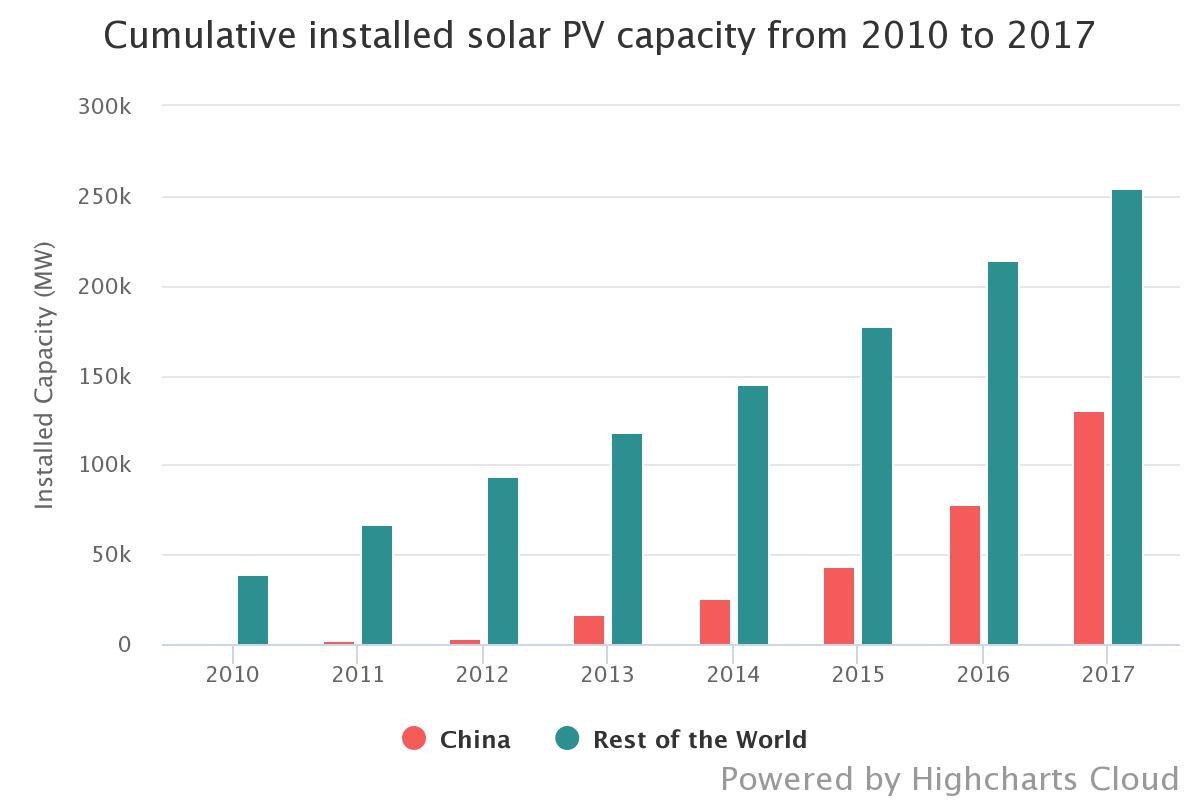

China has led the world in new solar installations in each of the past five years, helped by guaranteed electricity prices. But the cost of subsidies has been growing unsustainably, and as manufacturers have expanded rapidly to meet demand the risk of overcapacity has grown.

The new policy brings the industry to a crossroads. During the 12thFive Year Plan period (2011-2015) subsidies were paid late and there was significant wastage of both solar and wind power. Those lessons should have been learned by now, says Meng Xiangan, deputy director of the China Renewable Energy Society. To avoid a repeat, the sector can either lobby for an extension of subsidies and continue its rapid and unsustainable expansion, or accept that new capacity will face a tougher challenge on costs.

Source: IRENA

A sudden change

Under the current system, the National Energy Administration (NEA) sets annual targets for installed solar capacity, which is eligible for government subsidies. At the local level, development and reform commissions are responsible for approving projects. In theory, subsidies are limited to projects that fall within the NEA (central government) targets, although local governments may also provide subsidies.

The new policy, which came into effect immediately, has no target for the construction of solar farms, and orders local governments not to approve solar farms that need subsidising.

However, it is distributed solar projects, such as small-scale commercial and consumer rooftop installations that will see the biggest change. Previously, there was no target for distributed solar capacity, leading to strong growth in the distributed solar market.

In 2017, 19.44 gigawatts (GW) of new distributed solar was added – as much as the total for the previous three years. A further 7.68GW was added in the first quarter of this year, an increase of 217% year-on-year and 79.6% of all new installations in China. The new policy has put in place a target of 10GW of new distributed solar capacity (as oppose to solar farms), which means that the entire 2018 target was almost reached in the first three months of the year.

Alongside limiting the amount of new solar installations eligible for subsidy, the 531 policy also reduces the level of subsidy for solar farms and distributed solar, which were set through regional pricing policies in 2013.

These policies provided a huge stimulus for corporate investment in solar PV. They divided the country into three regions according to their suitability for solar generation, with prices paid per kilowatt hour set at 0.90, 0.95 and 1.00 yuan accordingly. Distributed solar installations were subsidised at 0.42 yuan per kilowatt hour.

The new policy has dropped those subsidies to 0.50, 0.60 and 0.70 yuan per kilowatt hour across the three regions, with the distributed solar subsidy falling to 0.32 yuan per kilowatt hour.

This is the second cut in subsidies in less than a year. In December 2017 the distributed solar subsidy fell from 0.42 yuan per kilowatt hour to 0.37 yuan.

“We were expecting subsidies to be cut back but this was too sudden and too sweeping, with no buffer period,” says a source at the Guangdong Solar Energy Association.

The cuts are a clear signal from government that the sector needs to become less dependent on subsidies and shift its focus from rapid scaling toward technological improvements to further bring costs down.

“The subsidy has been a major driver of new projects,” says Lin Boqiang, head of Xiamen University’s China Institute for Studies in Energy Policy.

“The idea of a subsidy is that eventually it goes away. China’s been slow to do that, it would have been better if this had happened earlier,” he adds.

A difficult transition

Many investors and project owners are waiting to see how the new policy plays out.

“Some customers immediately cancelled orders and demanded cheaper prices,” says Sun Yunlin, head of Winone Solar, which provides services such as consulting, feasibility studies and handover inspections to solar farms.

The market has dropped significantly. Wang Bohua, secretary general of the China Photovoltaic Industry Association, expects to see 30-35 gigawatts of new capacity in 2018, a drop of 43% on last year.

That drop in new installations in China means there is a risk of overcapacity in the supply chain, which has been expanding rapidly. The silicon subcommittee of the China Nonferrous Metals Industry Association calculates that China’s production capacity of polycrystalline silicon – a raw material for the solar industry – will reach 433,000 tonnes a year in 2018, growth of 57% year-on-year. Most of that new capacity will come on stream in the third quarter.

China’s percentage share of the solar PV industry in 2017 (Source: China Photovoltaic Industry Association)

A report from the China Centre for Information Industry Development (CCIDWise) predicts that growth in the solar PV market will fall off or even reverse, with further price drops to come across the industry and firms facing significant pressure on costs.

Wang Bohua, secretary general of the China Photovoltaic Industry Association, said at this year’s 3rd Century Photovoltaic Conference that expansion of manufacturing capacity was still rapid, but the warnings of overcapacity caused by excessive expansion back in 2011 should be heeded.

Mind the gap

China’s 13th Five-Year Plan (2016-2020) set a 105GW target for new solar PV capacity by 2020. This was hit two years and three months early. As of April 2018, capacity was 140GW.

One of the reasons for this runaway growth is because plans for the solar sector differ between central and local governments – particularly since the power to approve solar farms was devolved to the local level in 2013, which made it harder for central energy authorities to control the scale or rate of solar PV installations. That loss of control is why the subsidy funding gap has steadily widened.

“During the 12th Five-Year Plan the target for solar generation grew from 5GW to 10GW, then to 15GW, then ultimately from 21GW to 35GW. That was a bigger change than planned for any other industry. There was effectively no cap on total capacity,” explains Meng Xiangan.

The expansion started in 2013. The EU and US placed anti-dumping measures on imports of Chinese solar PV products, causing the overseas market to shrink. With no outlet for domestic capacity a meeting of the State Council in June that year took six measures to support the industry through the crisis: policy assistance, guaranteed purchase of solar power, improved electricity pricing policy, funding support, funding for research and design, and support for mergers and restructuring.

With guaranteed prices, solar power manufacturers and other companies started building solar farms. In December 2013 Deloitte published a report on clean energy in China that found 130GW of “queued” solar projects – three times the entire 12th Five-Year Plan target.

But the Renewable Energy Development Fund, from which subsidies are paid, had only one source of income – a renewable energy surcharge on electricity bills, which is collected by energy suppliers from customers. That surcharge has been adjusted five times and currently stands at 0.019 yuan per kilowatt hour.

Electricity prices were fixed while solar PV development costs fell

A key reason for the exponential growth in distributed solar PV installations in recent years is that electricity prices were fixed while solar PV development costs fell. This created enormous potential for profit, further encouraging investment in the sector.

This was particularly the case for distributed solar installations. The first adjustment was made in 2017 – a reduction of 11.9%, from 0.42 to 0.37 yuan per kilowatt hour. But during that same period the price of polycrystalline silicon panels (which make up 60% of the cost of solar installations) plummeted from 3.9 yuan per watt in 2013 to 2.4 yuan in 2018 – a drop of 38.5%. The cost of monocrystalline silicon panels fell to 2.5 yuan, dropping 37.8%.

That out-of-control growth left a huge funding gap in the subsidy scheme, which is now limiting the sector. Figures from the National Energy Administration show that as of the end of 2017 the accumulated shortfall in renewable subsidies stood at 112.7 billion yuan, with 45.5 billion yuan due to the solar PV sector. An extra 10 gigawatts in distributed solar means a further four billion yuan in subsidies has to be found – or 80 billion yuan over a 20-year period.

Hard to control

The National Energy Authority started trying to manage the expansion of the solar sector in 2014, but its goals didn’t align with the interests of local governments, so policies were not properly implemented.

To encourage investment, some local governments had a “first-built, first-served” policy – the first distributed solar installations to be finished were included in annual quotas, and thus eligible for subsidies.

Growth in solar has ‘been driven by business and local government’

Anhui made this explicit in a notice published in 2016, which stated that projects would be included in annual quotas in the order of their connection to the grid. This resulted in far more capacity being constructed than annual quotas allowed for – 2.55GW of new capacity was built in Anhui in 2016, compared to a quota of 0.5GW.

Wang Liguo and Ju Lei at Dongbei University of Finance and Economics have studied the roots of overcapacity in the solar sector.

They say: “it has been driven by business and local government, with the energy authorities forced to respond rather than guide and control the sector’s sustainable development.”

Better solar integration

Solar PV is still a key part of China’s low-carbon strategy, which is itself important for realising China’s commitment to reducing emissions and increasing the proportion of non-fossil fuel energy in the overall mix to 15% by 2020. But too much focus on installed capacity can come at the cost of coordinated planning across central and local government, and with the grid. This can add to the challenge of absorbing new solar capacity effectively into the power system.

This is evident in China’s north-west where 40% of the country’s total PV capacity is concentrated in five provinces (Shaanxi, Gansu, Qinghai, Ningxia, Xinjiang). It is also where the most solar power is wasted.

Because solar installations were not coordinated with power grid construction, there grid has limited ability to absorb the extra power and connection to the grid has been difficult. National Energy Administration figures show that curtailment of solar PV was 19.81% across those five provinces – that is, one fifth of solar power capacity is being wasted.

The National Energy Administration wants to reduce curtailment to just 5% nationwide. But this will be no easy task.

Fan Bi, former head of the General Economy Department at the State Council’s Research Office, has written that the intermittent nature of solar power causes problems if large scale, concentrated generation needs to be connected to the grid. Ultra-high voltage lines can be used to carry the power 1,000 and more kilometres to eastern and central China, but energy loss through transmission and transformation makes this a hugely uneconomical option for the State Grid.

And the provinces which would receive that renewable energy aren’t keen either, as they view it as against the interests of their own utility companies.

Dafeng power station in Yancheng, Jiangsu province combines wind power and solar PV (Image: Greenpeace/Zhiyong Fu)

Lack of a quota system

Guaranteed electricity prices incentivised the development and roll-out of renewable energy, but they didn’t create demand for that power. There needs to be a better balance between the varying interests on the grid, power generators, and consumers to ensure a atable market.

One approach to rectify this was detailed in March this year by the National Energy Administration, which plans to establish a renewable energy quota system. This would require each province to source a certain percentage of electricity from renewables, passing the cost of the quota obligation onto market actors (such as power networks, electricity suppliers and major electricity consumers).

But there is uncertainty over the quota system already. The government’s work report at this year’s Lianghui called for large reductions in the non-taxation burdens on companies, and specifically for “reductions in power distribution and transmission network charges, with ordinary industrial and commercial electricity costs falling 10%”.

Lin Boqiang says a renewable energy quota system could prevent the waste of solar power, but it would mean higher prices. With the government hoping to boost business competitiveness, it may be reluctant to implement the proposed changes.

Back to the market

Responding to questions on the new 531 policy, the National Energy Administration said that it will encourage firms to shift their reliance from government policy to the market. This is expected to help eliminate excess capacity, encourage technological improvements, end the sector’s irrational expansion, and concentrate resources in stronger firms.

After an initial panic, the industry is now calmer about the future. “At Guangdong electricity prices, solar PV is a viable investment if solar cells drop in price to 1.8 to 2 yuan per watt. We expect to see 2 yuan per watt at the end of the year,” says Sun Yunlin from Winone Solar.

Li Chuangjun, deputy head of the new and renewable energy department at the National Energy Administration agrees that the cost of solar is reaching parity with conventional technologies. He says that technological advances have seen costs fall by about 90% from 2007 to 2017, and power from solar PV may be sold to the grid at standard rates within two or three years.

Some industry insiders are even more optimistic. Four days prior to the release of the 531 policy Liu Hanyuan, chair of the Tongwei Group, said at the 12th International Solar and Smart Energy Exhibition that innovation and further economies of scale could help solar match coal-fired power on a cost basis across most of China.

Meng Xiangan says it is now time for the sector to “find its place in the overall market”.

The article was produced jointly by chinadialogue and Energy Observer. This version has been edited from the Chinese original. This article is republished from chinadialogue.