Image: ADB Flickr account

On August 7, the government of Laos officially suspended consideration of all new dams in order to review its hydropower strategy in response to the safety vulnerabilities exposed by the tragic collapse of the Xepian Xe Namnoy Dam in Laos on July 23. This is a turning point for the Lao leadership, who have long pinned hopes for Laos’s development on being the “Battery of Southeast Asia” by exporting hydroelectricity to markets in neighboring markets in Thailand and Vietnam.

This pause creates a window of opportunity for Laos to reconsider the dominant role of hydropower in the country’s energy mix at the same time as alternative and less risky energy sources such as solar, wind, and biomass are becoming economically competitive options. Transitioning to a more diverse mix of energy would provide put Laos on the path towards being a greener “battery” and would ultimately greatly reduce food security, environmental, and natural disaster risks to the Mekong region as a whole.

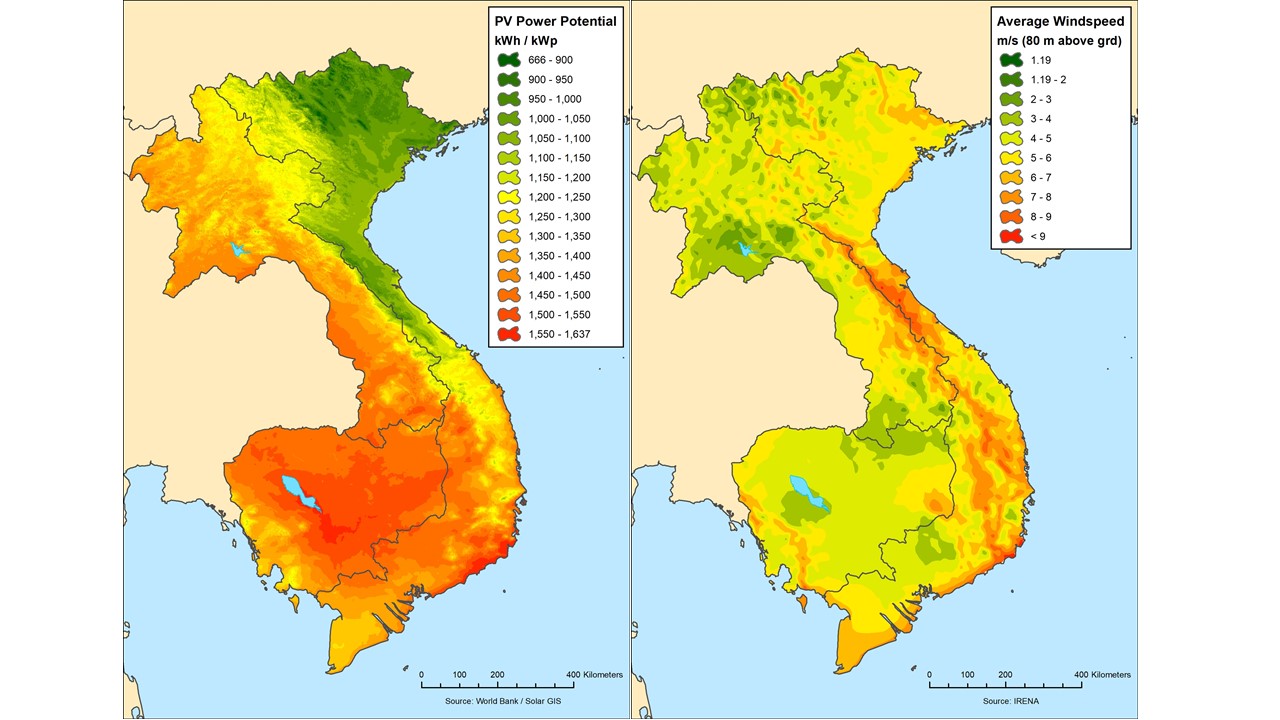

The dam breach happened at a point where the government of Laos still has an opportunity to choose a different and more sustainable path: only approximately 6,000 MW of a potential 18,000 MW of technically feasible hydropower dams have been constructed inside the country. An additional 5,000 MW of dams are now facing a construction pause for safety examinations, and some—like the Pak Beng Dam—are paused due to uncertainty on the part of the power purchaser. Ultimately, this is still only a portion of the Lao government’s goal planned full buildout and opens the door to meeting export goals through a more diverse mix of alternative options. Laos has approximately 8,800 MW of solar potential, and another 2,200 MW of high quality wind potential. There is significant scope for Laos to take advantage of the dropping prices in reconsidering the makeup of its future energy mix.

Solar (left) and wind (right) endowments for Laos, Cambodia, and Vietnam.

Non-hydropower renewable options are gaining traction globally. The prices of utility-scale solar and wind have dropped approximately 85% and 65% respectively since 2009, and this drop is continuing. Utility-scale solar price in the United States dropped 30% from 2016 to 2017, and bids on solar and wind plants around the world regularly set new records: since 2017, we’ve seen solar lows in the United States of 2.3 c/kWh, in India of 3.6 c/kWh, and the UAE at 2.94 c/kWh while Mexico signed a contract for wind at 1.77 c/kWh and Saudi Arabia saw bids as low as 2.1 c/kWh for its first onshore wind project. In many cases, these records are not only for new low solar prices but for low overall electricity price.

The rise of renewables is already impacting Laos’s neighborhood: Thailand’s solar capacity has more than doubled since 2014 to more than 3,300 MW, and Thailand’s wind capacity is just over 600 MW as of late 2017. This puts Thailand more than halfway towards its 2036 solar target of 6,000 MW, a fifth of the way towards its wind target of 3,000 MW, and squarely establishes it in the leading position for new renewables in all of ASEAN. Thailand’s Ministry of Energy has already raised the 2036 non-hydro renewable energy target from an original target of 20% to 30 and has dropped a Feed-in-Tariff that stimulated growth in the sector to only 7.2 c/kWh, which is close to grid parity pricing. Thailand’s adoption of clear policy has made a clear business case for investment, which is why Thai companies plan to invest $3.9 billion in non-hydro renewables in 2018.

The policy and financing environment in Laos and Cambodia is not yet as welcoming or conducive to these record prices, and the local low prices for pilot solar projects currently stand around 8 – 9 c/kWh. However, significant price drops in these less mature markets is only a matter of time and depends largely on the timeframe for regulators clarifying the policy framework and opening bids for competitive tender. As the investment environment improves and perceived risk of these projects drops, financiers will begin offering better loan terms. On average, open auctions drop selling the price of electricity by 35 – 50% just in the first year by increasing competition for the tenders and pushing companies to cut costs. It is not unlikely to expect that prices in Laos would follow this trend if supportive policies were adopted.

Internationally and on a levelized cost of electricity, unsubsidized solar and wind are both already outcompeting coal. New commercially-viable hydropower projects in Laos, which are often more technically difficult and remote than earlier and cheaper projects, are coming online upwards of 7 c/kWh. Even a conservative price drop of one third in the solar price in Laos would put solar in a competitive position vis-à-vis new hydropower. A power expansion study led by experts at UC Berkeley’s Energy and Resources Group indicates that the least-cost development scenario for Laos’s power grid through 2030 would start replacing hydropower with a mix of wind, solar, and biomass by 2021. This more diverse scenario would avoid most planned dams and coal plants and would need $2.6 billion less investment than the business-as-usual scenario under the current government inventory of projects.

The price drops both make solar and wind more financially attractive and raise questions about the long-term competitiveness of planned hydropower and coal projects in a rapidly changing regional energy market. Laos’s development plans depend on the sale of electricity to markets abroad, and a shift in the way that buyers in Thailand and Vietnam think about their power mix is may have long-term implications for Laos. Thailand’s success with renewable energy is spurring a re-think of the national power development plan, and planners may consider replacing imports from comparatively expensive and controversial hydropower from Laos with domestically available renewable energy. Some experts have indicated privately that Thailand may significantly reduce its plan to purchase 10,000 MW of power from Laos.

If Thailand is out of the buying market, Vietnam is the only other neighbor with the capacity to buy from Laos’s battery—and Vietnamese stakeholders are understandably reluctant to purchase from hydropower which will have devastating impacts on the agriculturally productive and economically important Mekong Delta. At the same time, Vietnam’s energy demand is still high even in a region facing skyrocketing energy demand due to urbanization and industrialization.

Therein lies a contradiction as well as an opportunity: there is no reason that Vietnam cannot increase its power purchase from Laos as long as it is purchasing from a diverse and sustainably developed portfolio of power projects. The pause on new hydropower development in Laos provides an opportunity not only to the government of Laos to diversify its electricity supply, but also for policymakers in Vietnam to protect the Mekong Delta without infringing on the sovereignty of its neighbor. If Vietnam were to support investment and sign power purchase agreements for a mix of strategically sited dams and non-hydropower renewables, it could provide Laos with much-needed revenue and meet its own energy needs in southern Vietnam by negotiating to replace the worst-performing dams with wind and solar projects.

Taking the off-ramp from the business as usual, hydropower-heavy scenario is very possible for Laos because investor interest in this alternate portfolio already exists even though Laos has not yet adopted policies that lay out a clear pathway for non-hydropower renewable investments. Thai company Impact Energy Asia is pursuing a 600 MW wind farm in southern Laos, American company Convalt Energy is moving ahead with 300 MW of solar and is in talks for up to 700 MW more, and many investors are expressing interest in “floatovoltaic” solar plants that would sit on reservoirs in central and southern Laos.

The pause on hydropower construction provides the time for Lao officials to work with neighbors in Vietnam to hammer out what an alternative future would look like and lay out directions and a map to get there. Doing so would avoid risks, position Laos to be a greener and more sustainable long-term “battery” for regional development, and would ultimately mitigate long-term food, water, and security risks for the Mekong region as a whole.

Courtney Weatherby is a Research Analyst with the Southeast Asia program at the Stimson Center. Her research focuses on infrastructure development, climate change, and energy issues in Southeast Asia, particularly the food-water-energy nexus in the Mekong River basin and China’s investment in regional energy infrastructure.

World’s largest solar maker invests in Yunnan

World’s largest solar maker invests in Yunnan Regional Roundup for Week of 6.16.16

Regional Roundup for Week of 6.16.16 China needs to change its energy strategy in the Mekong region

China needs to change its energy strategy in the Mekong region