Over the last two decades the improved bilateral relations between China and the Philippines led to the increased inflows of Chinese economic capital—as foreign direct investment (FDI) and aid—in the Philippines. I argue that China’s foreign aid, if managed correctly will immensely benefit the Philippines.

During the Arroyo administration (2001-2010), the number of Chinese aid projects ranging from commercial and concessional loans to grants increased exponentially. Some of these projects were ultimately cancelled such as the ZTE/North Rail projects, and CHED Cyber education projects while others like the Banaoang Pump Irrigation Project, General Santos Fishing Port Complex Expansion, and Agno River Integrated Irrigation project were successful yet publicly invisible. However, after the Aquino administration (2010-2016) mounted a legal challenge to China over South China Sea claims, Beijing halted new loans and aid projects.

Today Philippine President Rodrigo Duterte is pursuing a new approach with an eye on China’s Belt and Road Initiative (BRI), which aims to centralize investment and aid inflows at crucial geographies and sectors. During Duterte’s 2016 visit to Beijing, he received $24 billion in investment pledges to complement the administration’s massive $183 billion five-year Build Build Build (BBB).

I began my field research in the Philippines in 2014, focusing on Chinese foreign investments in the mining sector. Afterwards, I moved to studying Chinese foreign investment and aid in the Philippines more broadly. As such, I’ve been conducting field research on China’s $24 billion commitment to the Duterte administration and made the following preliminary findings.

First, pundits with alarmist tendencies populate major media and popularized a “debt trap” without ample empirics. There is no doubt that Chinese aid generated debt trap crises that have plagued high risk countries. In a debt trap, a country loses its output to loan payments, costing the country an opportunity to expand its output. Overwhelmed by spiraling debt service and low growth, the host country eventually loses control of collateral assets to the lender. Using credit risk ratings and the International Monetary Fund’s debt sustainability analysis, the Center for Global Development (CGD) finds that 23 out of 56 countries show reasonable levels of risk to China’s BRI.

However, the risk of a debt trap appears to be low in the Philippines largely due to its BBB and BA1 credit ratings. Indeed, the World Bank argues that debt traps are avoided if projects generate output that outpaces debt. There is a strong domestic demand for infrastructures due to internal activities, which will surely generate a multiplier effect for the Philippine economy. A common criticism is that the Philippines could acquire Japanese Infrastructure Construction Agency (JICA) loans at less than one percent.

However, JICA or ADB loans comprise already of more than half of present loans since October 2016 while there are only 3 projects to be funded by China thus far. Additionally, Japan cannot possibly provide loans to all infrastructure projects due to borrowing limitations, expediency, and environmental requirements. While there are some concerns around Chinese loans, these must be assessed against the opportunity cost of not funding the project.

Underpinned by continued strong macroeconomic fundamentals due to structural reforms begun under Aquino, Duterte’s economic team is well-positioned to balance growth and the debt to GDP ratio. The present list of projects does not present concerns of a debt trap. One such project is the Chico River Pump Irrigation Project in Northern Luzon for which in April 2018 the Duterte administration signed a $62 million loan agreement with 2 percent annual interest maturing in 20 years and a 7-year grace period. Two China grants, which are turnkey projects built by Chinese firms and labor for free or, have been signed for two Philippine bridges valued at $73 million. The Kaliwa Dam Project has passed bidding, with stakeholders and Chinese developers currently in consultation. Other projects in the pipeline are under study, including a South PNR Project, the Philippine SAFE, and 12 other bridges.

Other projects further down the line include the renovation of the Clark Airport and the second phase of the Mindanao Rail project. Indeed, the loans of Chico and Kaliwa dam are manageable while the bridge projects are for free. The two train projects and the airport are the riskiest in the list, presenting the strongest case for the debt trap, but these have not even begun yet. However, these risks can be minimized if these projects generate enough output, which could be used to pay for the borrowed loans. Some degree of inflation and deficit spending will increase due to increased import spending. One crucial concern is that the Philippines’ growth or output depends on moderate inflation and fiscal deficits. The “debt to GDP ratio” tends to shrink when inflation goes awry, which could lead to a deficit increase and the conditions of a debt trap. Additionally, aid projects from future commitments that would not generate sufficient output should be a cause of concern. These are issues that the economic managers of Philippine currency and infrastructure projects need to watch.

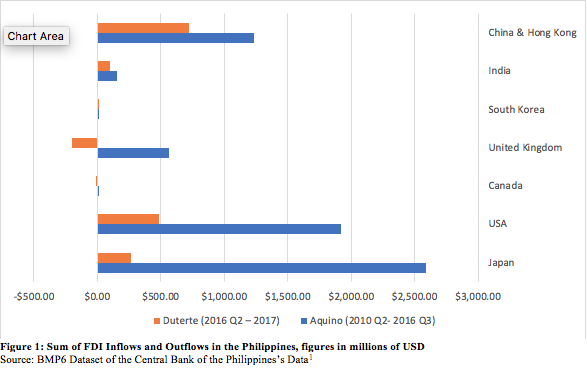

Second, host state factors matter to the completion or cancellation of China’s aid projects. For China, a Palgrave Communications study that finds a 10:1 ratio exists between pledges and actualization of investments. The ratio can be explained by various sending and host state factors, which means that the actualization of the entire pledged amount is highly unlikely. While Chinese FDI failed to reach the $15 billion pledged, between June 2016 and April 2018, Chinese FDI in the Philippines reached US$1.02 billion, amounting to nearly 85 per cent of the total amount registered during the Aquino administration. In other words, media and pundit outrage at the low amounts of Chinese actualized FDI should be taken with a grain of salt given the expected rate of cancellation from foreign commitments. Nonetheless, China should be criticized for the lack of transparency of aid and investment projects, and the Duterte government should be reprimanded for marketing pledged rather than actualized amounts.

On all Chinese and non-Chinese projects in the Philippines, elite competition, regulatory red tape, and local government decisions largely account for investment cancellation and delays. Currently, these host state factors are shaping the outcome of China’s $24 billion pledged. For instance, a hydropower project by Power China Guizhou and Philippines Greenergy Development Corp encountered trouble acquiring funds because of the uncertainty regarding the recently signed Bangsamoro Basic Law (BBL), a law which grants autonomy to the Muslim areas of the Southern Philippines. Most of the major investment projects in Mindanao province have been delayed because of this new terrain as investors are trying to figure out the economic implications of the new law. In another, a deal between Global Ferronickel, the third-largest nickel ore producer in the Philippines, with Baiyin Nonferrous Group, a Chinese copper supplier that was put on hold due to a moratorium on new mining operations, which made investment in mining operations fruitless.

In other cases, the completion of Chinese projects also depends on the preferences and political sway of local elites, which often matter to project implementation, local government regulation, and popular compliance. Projects such as rail networks tend to take a long time to negotiate due to the unequal distributionary impact of the infrastructure, which will concentrate economic activity and political gain on cities with train stops. Other locations, which will only receive the rail tracks, will lose out relative to those receiving the stops. In other words, intense local elite competition typically occurs when rail projects manifest.

The foreign funder and national governments often need to distribute economic or political rent to receive elite compliance to the plans. To some degree, these issues occurred in HSR in Indonesia, the Eastcoast Railway Link in Malaysia, and the Sino-Thai Railway. This is also the reason why the PNR South Rail and Mindanao Rail projects are experiencing delays. Conversely, infrastructure projects that disburse relatively equal benefits to local elites generate compliance and project progression. Roads cut across numerous cities, airports create multiplier effects, and irrigation projects can be built across farms. As such, the road projects, the Kaliwa Dam, and the Chico Irrigation are steadily moving forward with local elite cooperation and have experienced delays on technical matters instead.

Ultimately, the improvement of macroeconomic foundations during Aquino, a high demand for infrastructures due to domestic activities, and a diversified list of funders minimize debt risk. I recommend that the Philippines and other states establish a new and independent BRI Review Board exclusively for Chinese projects. This board should receive support from international organizations and directly report to the most important institutions of the country. In addition, a review of policies by international development banks that aim to expedite the project funding process will make the banks more attractive alternatives for countries seeing infrastructure loans.

{kind=link}

_(Mahathir_cropped).jpg){kind=link}